Before you start cutting costs, raising prices, or chasing more revenue, there’s a step many business owners skip—and it’s the one that matters most:

Clarity.

You can’t fix what you don’t fully understand. Cash flow issues are rarely solved by guesswork. They’re solved by visibility into how money actually moves through your business.

Let’s break down the key metrics you need to understand before making any changes.

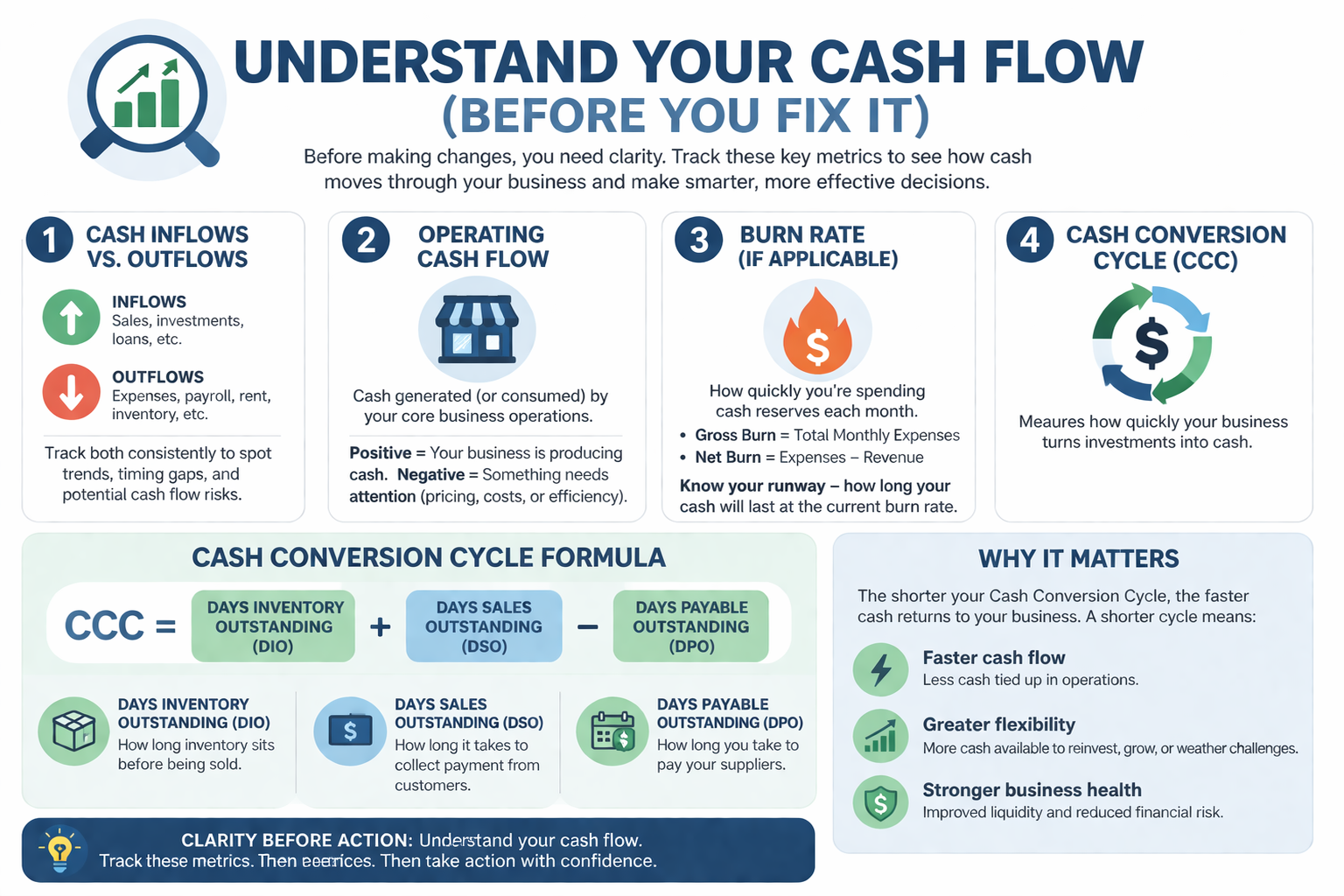

1. Cash Inflows vs. Outflows

At the most basic level, cash flow is simple:

- Inflows: Money coming into your business (sales, investments, loans)

- Outflows: Money leaving your business (expenses, payroll, rent, inventory)

But the real insight comes from tracking these consistently over time.

Ask yourself:

- Are inflows predictable or inconsistent?

- Do outflows spike at certain times of the month or year?

- Is there a growing gap between money in and money out?

A profitable business can still run out of cash if timing is off. That’s why this is your foundation.

2. Operating Cash Flow

Operating cash flow tells you how much cash your core business operations generate.

This strips away financing and investing activities and answers a critical question:

Is your business itself producing cash—or consuming it?

Positive operating cash flow means your business model is working.

Negative operating cash flow means something deeper needs attention—pricing, costs, or efficiency.

3. Burn Rate (If Applicable)

If you’re in a startup or growth phase, burn rate is essential.

Burn rate = how quickly you’re spending cash reserves

There are two types:

- Gross burn: Total monthly expenses

- Net burn: Expenses minus revenue

This tells you your runway—how long you can operate before needing more cash.

Without understanding burn rate, you risk making reactive decisions too late.

4. Cash Conversion Cycle (CCC)

This is where things get more strategic.

The Cash Conversion Cycle (CCC) measures how quickly your business turns investments (like inventory) into actual cash.

Formula:

CCC = Days Inventory Outstanding + Days Sales Outstanding – Days Payable Outstanding

- Days Inventory Outstanding (DIO): How long inventory sits before being sold

- Days Sales Outstanding (DSO): How long it takes to collect payment

- Days Payable Outstanding (DPO): How long you take to pay suppliers

Why the Cash Conversion Cycle Matters

The CCC reveals how efficiently cash flows through your business.

- A shorter cycle means you recover cash faster

- A longer cycle means your money is tied up longer in operations

For example:

- If you hold inventory too long → cash is stuck on shelves

- If customers take too long to pay → cash is stuck in receivables

- If you pay suppliers too quickly → cash leaves your business sooner than necessary

The goal:

Shorten the time between spending cash and getting it back.

Clarity Before Action

Most businesses jump straight to solutions:

- “We need more sales”

- “We need to cut expenses”

- “We need funding”

But without understanding these core metrics, those decisions can miss the real problem.

Cash flow issues are often about timing, efficiency, and structure—not just volume.

Final Thought

Before you try to fix your cash flow, map it.

Track it.

Break it down.

Understand the story your numbers are telling.

Because once you have clarity, the right actions become obvious—and far more effective.